Why a Prorated Rent Calculator for Move-In Can Save You Hundreds

Using a prorated rent calculator move in tool is the fastest way to know exactly what you owe when your lease starts on any day other than the first of the month.

Quick answer — how to calculate prorated rent at move-in:

- Divide your monthly rent by the number of days in the move-in month to get your daily rate

- Count the number of days you’ll occupy the unit (including your move-in day)

- Multiply the daily rate by those days to get your prorated amount

Example: $1,500 rent ÷ 31 days = $48.39/day × 17 days = $822.58 prorated rent

Moving into a new place mid-month is exciting — but the math that comes with it? Not so much.

Your landlord hands you a move-in cost sheet. There’s a number labeled “prorated rent.” It might be right. It might not be. And if you’re not sure how to check it, you could end up overpaying without even knowing.

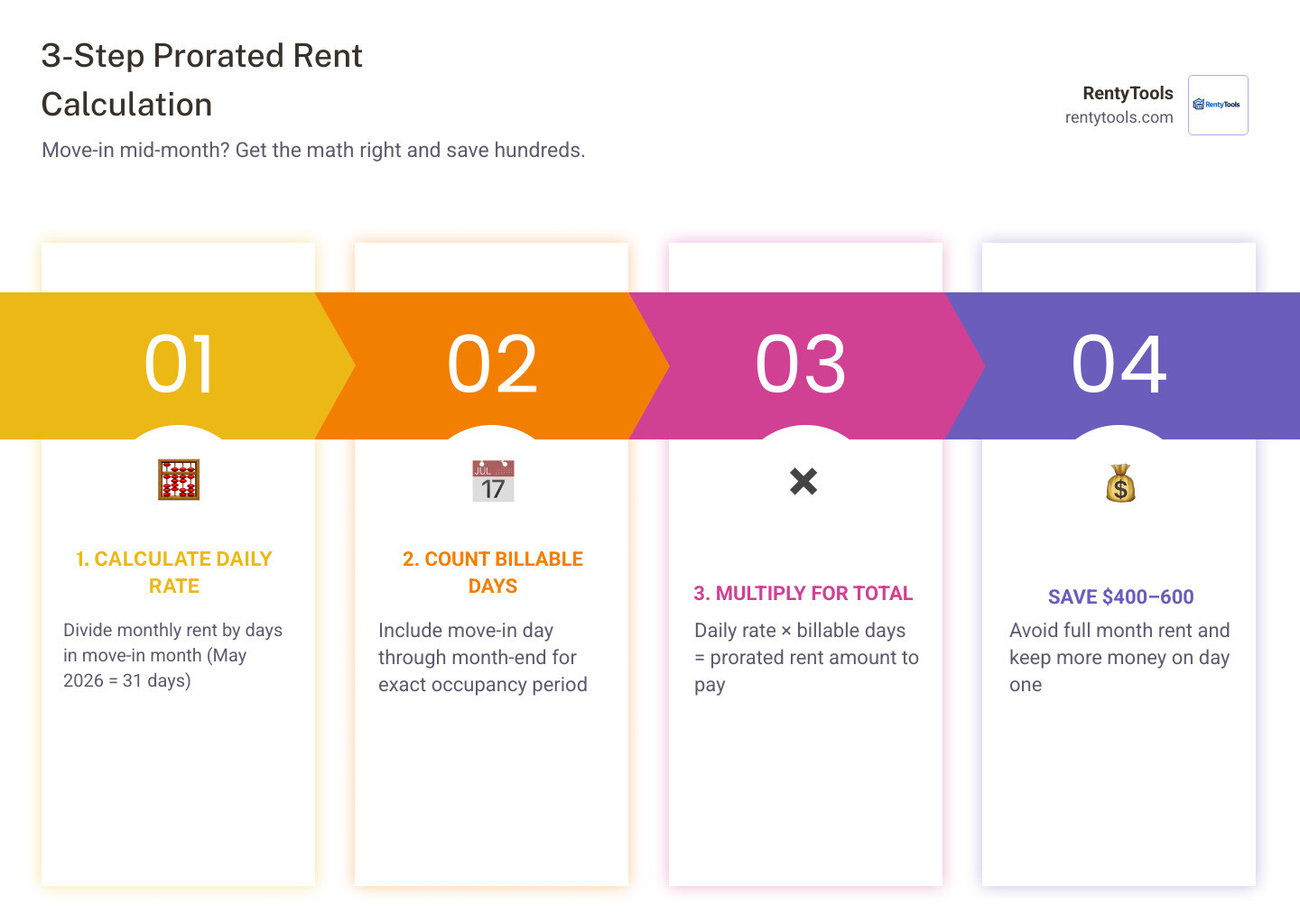

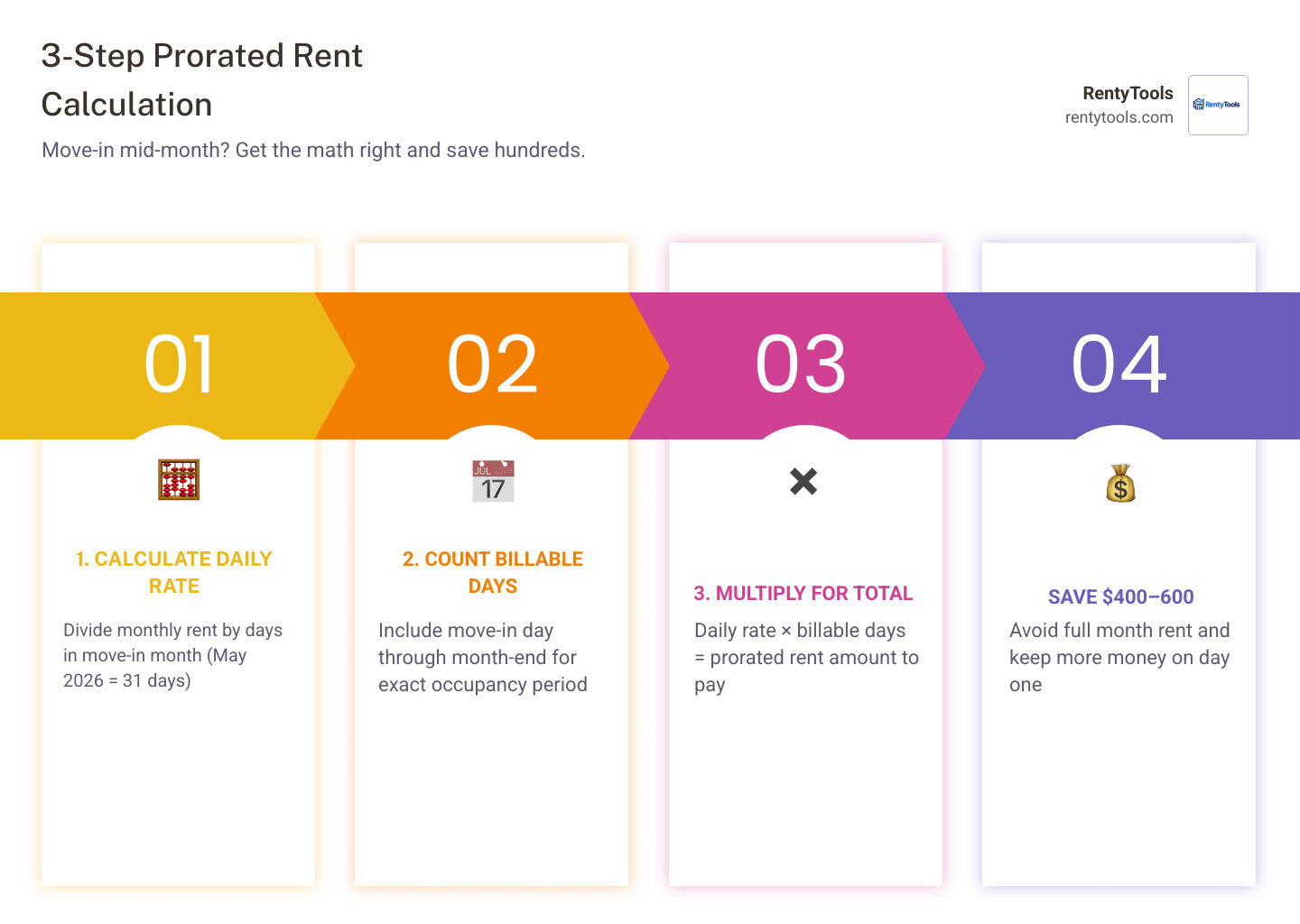

That’s a real problem. Mid-month move-ins are common, and the difference between paying a full month’s rent versus a prorated amount can mean $400–$600 back in your pocket on day one.

The good news: the calculation is simple once you know the steps.

What is Prorated Rent and Why Does It Matter for Your Move-In?

At its core, “prorated” simply means divided proportionally. In the rental world, prorated rent is the amount you pay when you only occupy a property for part of a standard billing cycle.

Imagine it’s May 2026. You’ve found the perfect apartment, but the current tenant isn’t out until the 10th, and you’re scheduled to move in on the 15th. Should you pay for the 14 days the apartment was empty or occupied by someone else? Absolutely not.

Prorated rent ensures you only pay for the days you actually have the keys. This is vital for several reasons:

- Significant Savings: On average, prorating rent for a mid-month move-in saves tenants between $400 and $600 compared to paying a full month’s rate.

- Fairness: It creates a transparent, logical system where neither the landlord nor the tenant is “gaming” the other.

- Faster Move-ins: Research shows that landlords who offer prorated rent fill their vacancies up to 30% faster. It removes the financial barrier for a tenant who might otherwise wait until the 1st of the next month to save money.

- Professionalism: Over 70% of modern rental leases now include explicit terms for proration. Using a standard method helps build a positive landlord-tenant rapport from day one.

For a deeper dive into the financial benefits, check out Why Prorated Rent for the First Month Can Save You Real Money.

How to Use a Prorated Rent Calculator for Move In: A 3-Step Guide

While you can do the math on a napkin, using a digital prorated rent calculator move in tool is the best way to ensure accuracy to the penny. Here is the foolproof 3-step process we use at RentyTools to get the right number every time.

Essential Inputs for a Prorated Rent Calculator Move In

Before you start clicking buttons, gather these four pieces of information:

- Monthly Rent Amount: The full price you agreed to in the lease.

- Move-In Date: The exact day you get possession of the unit.

- Days in the Month: Does the month have 28, 29, 30, or 31 days? (For May 2026, it’s 31).

- Billing Start Date: Usually the 1st, but some landlords use different cycles.

You can find specialized tools for these scenarios in our Rent Calculators section.

Step 1: Determine the Daily Rental Rate

The first step is finding out what one day of living in your new home costs. This is called the “Daily Rate.”

The most common method is using actual calendar days. You take your total monthly rent and divide it by the number of days in that specific month.

Formula: Monthly Rent / Days in Month = Daily Rate

For maximum accuracy, we recommend calculating this to four decimal places. Why? Because rounding too early can lead to discrepancies. If your rent is $1,000 in a 31-day month, the daily rate is $32.2581. While it seems like a tiny detail, those fractions of a cent add up when multiplied across two weeks!

Step 2: Calculate Total Billable Days

Now, you need to know how many days you are actually “buying.”

Crucial Rule: Always include the move-in day itself. If you move in on May 20th, you are occupying the unit for May 20, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30, and 31.

To find this quickly: (Total days in month – Move-in date) + 1 = Billable Days Example for May 20th: (31 – 20) + 1 = 12 billable days.

Step 3: Multiply and Finalize the Total

Finally, take your daily rate and multiply it by your billable days.

Formula: Daily Rate x Billable Days = Prorated Rent

Using our $1,000 rent example: $32.2581 x 12 = $387.0972. You then round this to the nearest cent, giving you a final total of $387.10.

By following these steps, you can verify your landlord’s math using our Prorated Rent Calculator.

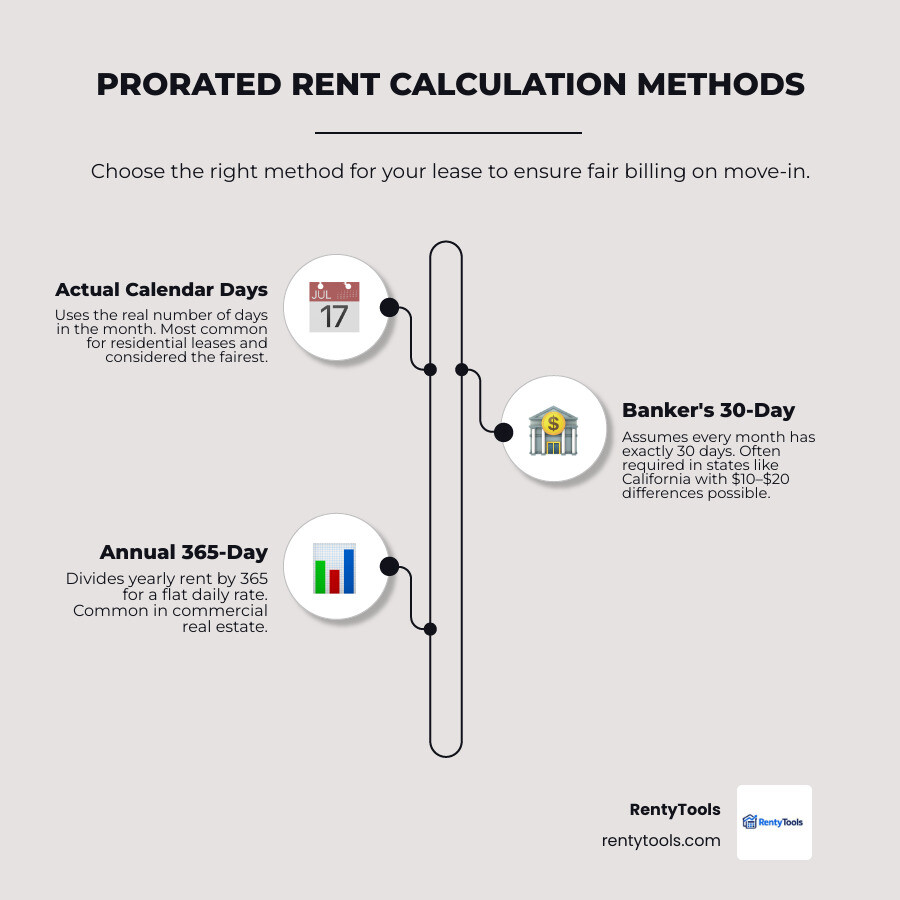

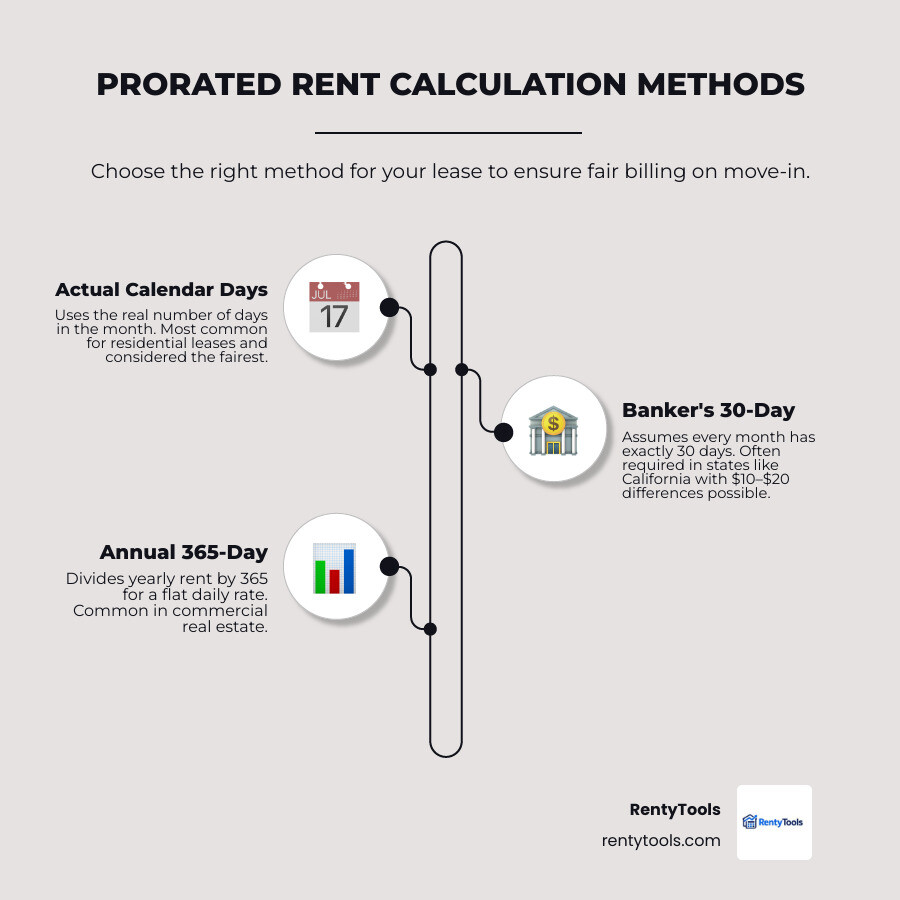

Comparing Calculation Methods: Actual Days vs. 30-Day Standard

Not every landlord uses the same “ruler” to measure time. Depending on your lease or your state’s laws, the math might shift slightly.

MethodHow it WorksExample ($1,500 Rent, March 15 Move-in)Actual Calendar DaysUses the real number of days in that specific month (28-31).$1,500 / 31 days x 17 days = $822.58Banker’s 30-DayAssumes every month has exactly 30 days.$1,500 / 30 days x 17 days = $850.00Annual 365-DayDivides yearly rent by 365 to find a flat daily rate.($1,500 x 12) / 365 x 17 days = $838.36

Which one should you use?

- Actual Days: This is the most common standard for residential leases and is generally considered the fairest.

- Banker’s 30-Day: This is often required in specific states, like California. It simplifies accounting but can result in a $10–$20 difference depending on the month.

- Annual: Often used in commercial real estate or long-term corporate housing.

Always check your lease agreement to see which method is specified. If it isn’t mentioned, the “Actual Days” method is the industry default.

Beyond the Basics: Leap Years and Non-Standard Billing

Math gets a little “funky” when the calendar doesn’t play nice.

The February Factor

February is the most volatile month for proration. Because it has fewer days, the daily rate is higher.

- In a standard 28-day February, $1,500 rent costs $53.57 per day.

- In a 31-day month like May 2026, that same $1,500 rent costs only $48.39 per day.

If you move in during a Leap Year, make sure you divide by 29! Using 28 days when it’s actually 29 can result in you overpaying your landlord by a full day’s worth of rent.

Billing Dates Other Than the 1st

What happens if your rent is due on the 15th of every month, but you move in on the 1st? This creates a “partial period” that spans two different months.

In this scenario, you have to calculate the daily rate for each month involved.

- Calculate the daily rate for the remaining days of Month A.

- Calculate the daily rate for the initial days of Month B.

- Add them together.

Our prorated rent calculator move in tool handles these “two-month spans” automatically, so you don’t have to worry about the fluctuating day counts between, say, August (31 days) and September (30 days).

Verifying Your Total Move-In Costs and Avoiding Mistakes

Prorated rent is usually just one line item on a much larger bill. When you move in, you’ll likely be asked for:

- The prorated first month’s rent.

- The full second month’s rent (many landlords require this upfront if you move in late in the month).

- A security deposit (usually equal to one full month’s rent).

- Pet fees or parking permits.

Important Note: Security deposits are never prorated. Even if you move in on the 31st of the month, the security deposit remains the full agreed-upon amount. This is a fixed cost designed to protect the property, regardless of how many days you stay in the first month.

Common Mistakes to Avoid:

- Forgetting the Move-In Day: Some people subtract the move-in date from the total days (31 – 20 = 11) and forget to add the move-in day back in. You are living there on the 20th, so you owe for 12 days, not 11.

- Verbal Agreements: Never rely on a “handshake” for the prorated amount. Ensure the specific dollar figure is written into the lease or a signed addendum.

- Wrong Month Length: Double-check if the month has 30 or 31 days. It’s a common “honest mistake” by landlords that can cost you $30–$50.

If you are moving in with roommates and need to figure out how to divide that prorated total, visit our guide on How to Split Rent Fairly.

Frequently Asked Questions about Prorated Rent

Is a landlord legally required to prorate my rent?

Surprisingly, in many states, the answer is no. Unless there is a state law (like in California) or a specific clause in your lease, a landlord could technically demand a full month’s rent. However, it is standard industry practice to prorate. If a landlord refuses, it’s often a red flag regarding how they will handle other issues down the road. Always negotiate this before signing the lease.

Does the prorated amount apply to my security deposit?

No. As mentioned earlier, security deposits and move-in fees (like application fees or key deposits) are fixed costs. Proration only applies to the recurring time-based charge: the rent.

Conclusion

At RentyTools, we believe that financial transparency is the key to a stress-free rental experience. Moving is expensive enough without overpaying for days you haven’t even spent in your new home.

By understanding the “Daily Rate x Billable Days” formula, you can step into your new apartment with the confidence that you’re paying exactly what is fair. Whether you’re dealing with a leap year, a 31-day month, or a non-standard billing cycle, our Prorated Rent Calculator is here to do the heavy lifting for you.

Run the numbers, verify your lease, and keep that extra $500 in your pocket for the things that really matter—like that new sofa or a celebratory “move-in day” dinner!